The digital underground, like any economy, relies on the free flow of funds. The variety of payment mechanisms available to and used by cybercriminals is diverse. It ranges from real world, physical payments to untraceable cryptocurrencies, and everything that falls in between. Many payment mechanisms with a significant or absolute online aspect offer a number of features that make them attractive as a financial instrument for criminal enterprise – anonymity, rapid, cheap and irreversible transfers, and obfuscated financial transactions. In many respects, some payment mechanisms can offer a level of anonymity similar to cash but in an online environment.

The payment mechanisms used by cybercriminals can be broken down into the following categories:

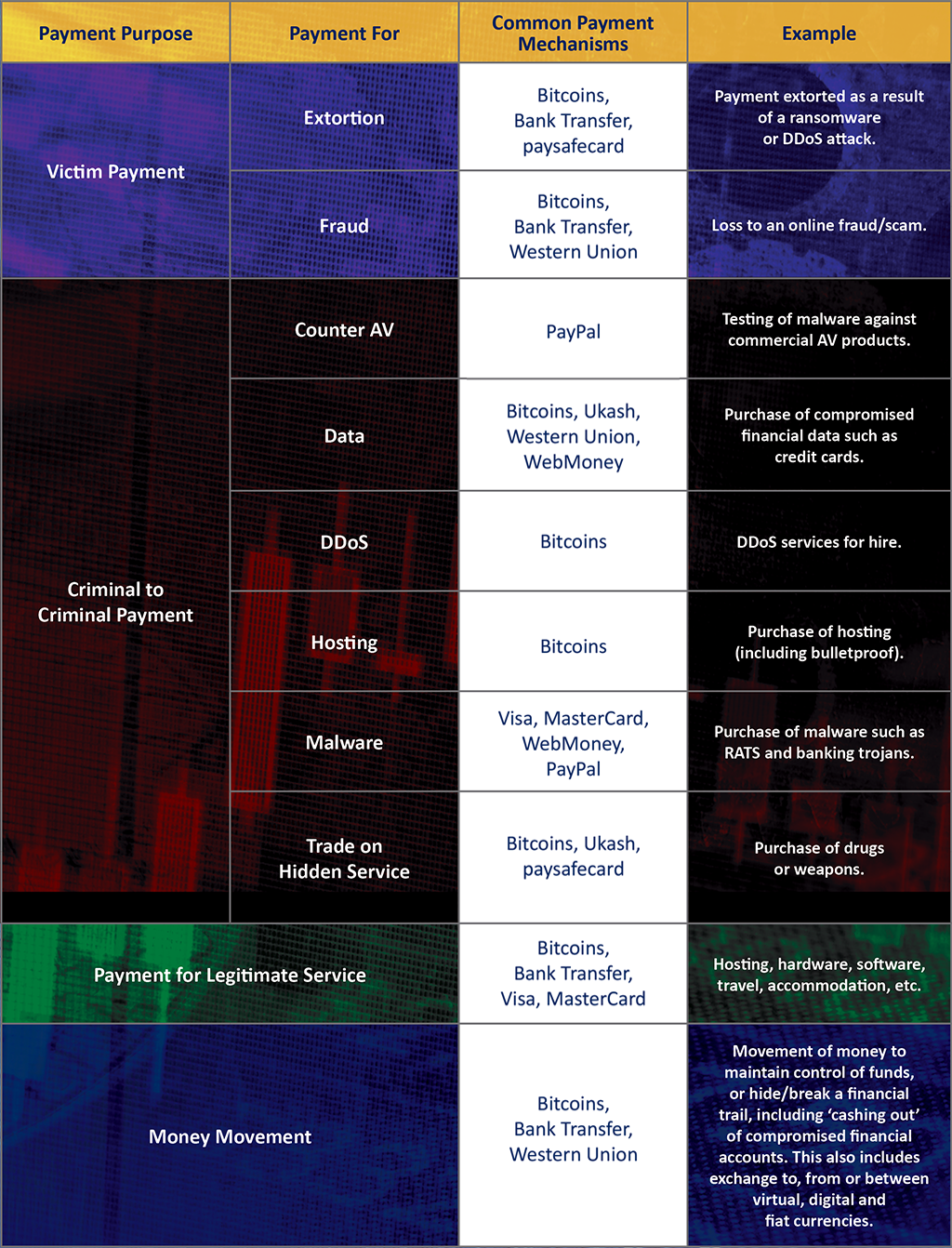

Furthermore, when considering how and why cybercriminals use any particular payment mechanism it is important to consider the nature of the transaction. In this respect, four distinct scenarios can be identified.

Click here to open this table

Click here to open this table